Last week, Shanghai aluminum prices fell back to the previous consolidation area to gain support. The main contract AL0611 closed at 19,290 yuan/ton, which was a decrease of 910 yuan or 4.5% from the previous week. The market continued to maintain the price structure of long-term contracts, showing near-strong strength. Aluminium fell sharply, closing at $2445 a week, down $190. The price of alumina continued to fall and the export tax rebate rate was lowered to suppress the aluminum market.

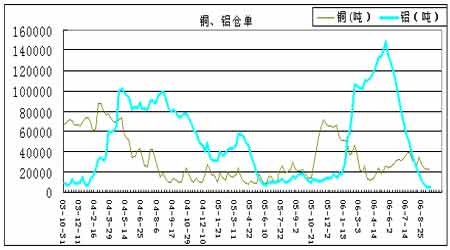

The low inventory era is coming. The pre-stock pressure turned into a downward momentum. This process is nearing completion and the low inventory will shift to supporting price action. As of September 15, the total volume of deliverables of aluminum stocks in the previous period was 25,762 tons, an increase of 4,355 tons, and 4,580 tons of registered warehouse receipts, a decrease of 147 tons from the previous week. After a fifteen-week continuous decline, the amount of deliverable goods increased slightly. , while registered warehouse receipts are for seventeen consecutive weeks. In the past two weeks, the resources of Shanghai Aluminum increased, and the decline in warehouse receipts was limited. After the pressure on resources is shown to be greater, it is significantly reduced, inventory resources are rapidly declining, and the outflow rate is greater than the inflow rate. The high level of warehouse receipts this year far exceeded the high level of last year's warehouse receipts, indicating that electrolytic aluminum production capacity has recovered rapidly and the market supply is sufficient. Manufacturers have significantly increased their efforts to preserve the value of the futures market. Last weekend, LME aluminum stocks were 705,000 tons, a slight decrease. Huge amount of warehouse receipts poses pressure when prices rise, but with the advent of the consumer season, demand has increased, and warehouse receipts have begun to flow out into the consumer sector and will continue to push down inventory.

Spot aluminum prices fell sharply, reflecting the demand for consumer season. As of September 14th, the price of spot aluminum ingots in the Yangtze River region in Shanghai closed at RMB 20,680/ton, down by more than RMB 2000 from last week. The general decline in the prices of metals such as copper and aluminum, as well as the realization of bearish interest in the reduction of export tax rebates, has led to a simultaneous drop in the current and current aluminum prices. In the spot market, the Shanghai region still maintains a low inventory status. While the price falls into the range acceptable to consumer companies, the demand will be reflected. The price of the Guangdong market is slightly higher than that of Shanghai. Arbitrage trading between the two places has significantly narrowed the spread. The reason for the low inventory is that the domestic domestic aluminum prices have been oversold, the domestic and international aluminum price spreads have widened, and the general trade exports are profitable, which is conducive to the export of primary aluminum and increased the arbitrage between Shanghai and London. Moreover, due to the strong expectation of the market to reduce the export tax rebate rate for aluminum products during the year, the export of aluminum products has increased substantially. From January to July, the export of domestic aluminum materials was 632,000 tons, an increase of 62.2% year-on-year. Drive domestic demand for primary aluminum.

The price of imported alumina continued to operate at a low level. Affected by the continuous expansion of domestic alumina production capacity, the price of alumina has not yet shown signs of significant decline. Last week, the alumina price of the port was lowered to around RMB 3,500/ton. China Aluminum announced that it had lowered the spot price of alumina by 22.4% from August 31 to RMB 3,800 per ton from 4,900 yuan. Prior to August 7, Chinalco's alumina price was lowered by 13.3%. The drop in alumina prices is related to the release of domestic alumina production capacity. In general, due to the expansion of the electrolytic aluminum industry in China, the demand for alumina has increased. Since the start of production of some domestic alumina production capacity in March, the supply of alumina has increased significantly, and the growth rate has exceeded the growth rate of electrolytic aluminum, thus restraining its price to rise. According to statistics, from January to June, China's alumina production reached 5.95 million tons, an increase of 50.6% over the same period of last year. The output of electrolytic aluminum during the same period only increased by 18.1% year-on-year; at the same time, the import volume of alumina in China showed a declining trend. The direct reason was that domestic prices fell to low. In the international market price. According to customs statistics, alumina imports amounted to 7.02 million tons in 2005, an increase of 19.6% over the previous year; and in the first seven months of 2006, imports totaled 3.95 million tons, a year-on-year decrease of -6.8%.

The current decline in alumina prices has weakened the cost support of electrolytic aluminum. However, the recent increase in electricity prices has increased the production cost of electrolytic aluminum. The recent national sales price rose by 2.5 cents/degree. If the electricity consumption per 1 ton of electrolytic aluminum is calculated at 15,000 kilowatts, the cost per ton of electrolytic aluminum will increase by 375 yuan. Taken together, the average production cost per ton of electrolytic aluminum is roughly around 15,780 yuan. Compared with the current spot price, manufacturers have more room for profit.

From a fundamental point of view, in December last year, the domestic large-scale electrolytic aluminum producers jointly reduced production by 10%, which was the basic factor that led to the drop in alumina prices and the rise in electrolytic aluminum prices. At the same time, reducing production also supports aluminum prices. However, with Shanghai Aluminum prices rising, the attraction to aluminum resources has increased, leading to a rapid increase in the number of warehouse receipts, the rapid increase in the amount of Shanghai aluminum resources and warehouse receipts, the rapid recovery of aluminum production capacity, aluminum spot supply is abundant, the domestic aluminum plant maintenance efforts Increased. At the same time, the new alumina production capacity has eased the tight supply of domestic alumina, and it can be said that the high inventory and cost reduction are the main factors for the continued decline in aluminum prices in the current round. We believe that the persistent contradiction between the growth in demand and overcapacity in the domestic electrolytic aluminum industry will remain the dominant factor in aluminum price changes. The decline will have cost support (limited decline in alumina prices and rising electricity prices) and aluminum demand support. Rising will cause the contradiction between demand austerity and excess production capacity, and will inevitably encounter high inventory pressure. The way to break the stalemate lies in the active shrinkage of the aluminum industry. As a result, aluminum prices will rise again; or the macroeconomic slowdown, and the total aluminum demand will decline, the current aluminum trend will reverse. If the two conditions are difficult to see in the short term, the aluminum price will maintain a turbulent process.

In the second half of the year, China will continue to implement austerity measures, and the real estate industry with large consumption of aluminum products will be restrained. On August 19, the Central Bank announced the increase of deposit and lending rates, raising the one-year deposit and loan interest rate by 0.27 percentage points; on July 21, the People's Bank of China decided to raise the deposit reserve ratio of depository financial institutions by 0.5 from August 15, 2006. percentage point. The loan interest rate was raised by 27 basis points on April 28, 2006, and the reserve requirement ratio was raised by 0.5% in mid-June. The rumors of lowering the export tax rebate rate for aluminum products (processed profile products) turned into facts last week, and the reduction in aluminum products was only 2%-5%. Compared with the previous 13% tax rate, at least 8% tax rebate is also enjoyed. To some extent eased the market's excessive pessimism.

The aluminum market has undergone substantial ups and downs, highlighting that the rising base is not solid. The reasons for the rise came from the fact that inventory pressure was weakened, and low inventory levels and strong export data from aluminum extrusions played a supporting role. At the same time, the technical strength of metals led by copper has not changed; but after the big rise, negative factors are exposed. On the one hand, the macro fundamentals are not conducive to the rise in metal prices. With the sharp drop in crude oil and the appreciation of the US dollar, metal prices are generally under pressure. The continued decline in alumina led to a further downward shift in the cost of electrolytic aluminum, as well as a reduction in the export tax rebate rate. Technically, Shanghai Aluminum has gained support in the near-term consolidation area, showing a technical adjustment trend. The late oscillation is not clear, and the possibility of overhang is slightly greater.

Basics:

Shanghai aluminum resources increase, warehouse receipts decline is limited

As of September 15th, the volume of deliverables for aluminum stocks in the previous period was 25,762 tons, an increase of 4,355 tons, and 4,580 tons of registered warehouse receipts, which was 147 tons less than the previous week (see the chart below). After a drastic decline in fifteen weeks, it was ready for delivery. The volume of goods increased slightly, while the registered warehouse receipts fell for seventeen consecutive weeks. In the previous period, as Shanghai Aluminum prices rose, the attraction to aluminum resources increased, resulting in a rapid increase in warehouse receipts, which was once higher than last year's warehouse receipts. As the aluminum inventory and registered warehouse receipts have been significantly reduced for fifteen consecutive weeks, and entered the era of low inventory, the recent increase in Shanghai aluminum resources, warehouse receipts decline is limited.

Figure 1: Copper and aluminum weekly warehouse receipts on the Shanghai Futures Exchange

China's iron and steel electrolytic aluminum and other 11 industries overcapacity issues list

At the end of 2005, the National Development and Reform Commission of China stated clearly that there were problems with overcapacity in 11 industries such as steel, electrolytic aluminum, and automobiles. Among them, overcapacity issues have highlighted seven industries, namely steel, electrolytic aluminum, automotive, ferroalloy, coke, calcium carbide, and copper smelting industries; and four industries with potential excess capacity, namely cement, electricity, coal, and textiles. The following is the basic situation of overcapacity in the above industries organized by Reuters according to China's official data:

Overcapacity issues highlight the industry

1. Steel:

Luo Bingsheng, executive vice president of the China Iron and Steel Association, said at the end of July that the excessively rapid growth of China's steel production in the first half of the year should attract attention. At the same time, the current situation of the steel industry's continuous increase in production capacity should be controlled. Capacity is still the current important task.

- The National Development and Reform Commission and relevant departments issued the "Circular on the elimination of the total amount of control of the steel industry to eliminate backwardness and accelerate structural adjustment" in June, pointing out that the contradiction between overcapacity in the steel industry is very prominent. By the end of 2005, it had formed 470 million tons of steelmaking capacity, 70 million tons of capacity under construction, and 80 million tons of proposed capacity. If it is completed, China's steelmaking capacity will exceed 600 million tons by the end of 2005. View consumption is about 350 million tons. Even considering the increase in demand for steel products in the future, supply and demand are seriously imbalanced.

- China Iron and Steel Industry Association recently said that in 2006 China's steel production will increase by 10%-15%.

2. Electrolytic aluminum:

-- The National Development and Reform Commission stated in late December last year that it will control the new capacity of electrolytic aluminum and limit the investment and redevelopment of related projects. - Zhu Hongren, deputy director of the Economic Operation Bureau of the National Development and Reform Commission, said at the end of January that the electrolytic aluminum industry had a capacity of 10.3 million tons, and the idle capacity was 2.6 million tons, and the company's loss was more than 60%.

According to statistics from the China Nonferrous Metals Industry Association, as of January 10, 17 of China's 23 large-scale electrolytic aluminum enterprises have started to reduce production, the rate of production cuts are all above 10%, cumulative reduction of production capacity is 335,000 tons, and another 380,000. Tonnes of new production capacity have been temporarily suspended. 23 companies have a production capacity of 6 million tons, accounting for 55% of China's total domestic production capacity.

3. Cars:

Chen Bin, deputy director of the Development and Reform Commission's Industry Department, said in December last year that at the end of the “Eleventh Five-Year Plan (2006-2010)â€, China’s auto production capacity could reach 20 million vehicles, more than double the actual demand.

-- Ma Kai, director of the National Development and Reform Commission, said in December last year that there was an excess capacity of 2 million vehicles and a capacity of 2.2 million vehicles under construction. The new capacity being planned and planned was 8 million vehicles.

- According to data from the National Bureau of Statistics, China produced 2,958,400 cars in 2005, a year-on-year increase of 26.9%. The overall vehicle profit decreased by 38.4%, and it is expected that the growth of car production and sales in 2006 will show a trend of rising from high to low, and the overall increase will be comparable to or slightly lower than in 2005.

4. Ferroalloy:

- Ma Kai, director of the National Development and Reform Commission, said in December last year that the current production capacity was 22.13 million tons, and the operating rate of the company was only about 40%.

-- The National Development and Reform Commission issued a notice early this year to implement industrial access inspections for ferroalloy production companies to curb blind investments in the ferroalloy industry and promote the upgrading of the ferroalloy industry.

5. Coke:

Officials of the National Development and Reform Commission said at the end of February that with the increase in the capacity to eliminate obsolete production, the problem of oversupply in the coke market is expected to ease to a certain extent this year, and the coke production capacity will remain at about 300 million tons in the next three years, which is currently approaching the coking industry. The bottom of the cycle, but the problem of excess will continue for 2-3 years.

-- Jin Qiang, chairman of the China Coking Industry Association, said at the end of February that by the end of 2005, the nation’s coking capacity was nearly 300 million tons and its capacity was about 24%.

-- Ma Kai, director of the National Development and Reform Commission, said in December last year that production capacity exceeded demand by 100 million tons, and that there were also 30 million tons of capacity under construction and proposed capacity.

6. Calcium carbide:

-- Ma Kai, director of the National Development and Reform Commission, said in December last year that the existing production capacity was 16 million tons and half of the capacity was shorted.

7. Copper smelting:

The Development and Reform Commission said at the end of July that starting from July 1, copper smelting projects newly built or reconstructed by the company must meet the requirements for single-system copper smelting capacity of 100,000 tons/year and above, and project capital ratios of 35% and above. condition.

-- Ma Kai, director of the National Development and Reform Commission, said in December last year that the total capacity of 2.05 million tons will be built and that by the end of 2007 it will have a capacity of nearly 3.7 million tons.

Exposed Rain Shower,3 Function Rain Shower,Copper Rain Shower,Black Exposed Rain Shower

Heshan Jasupi Sanitary Ware , https://www.jasupifaucets.com